Source: Morningstar Direct, Delta Research & Advisory

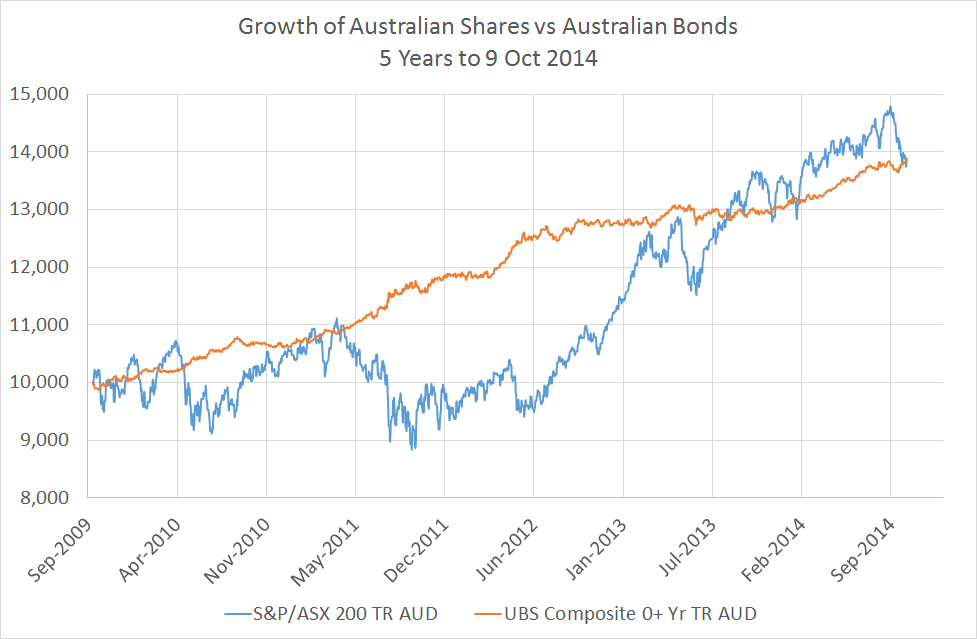

Over the last 5 years their performance has been pretty much the same…with the obvious exception that equities has bee a much much wilder ride. The reality of bonds in this global economy is that the outlook is still not that great from the major players (US, Japan, Europe, and in a sense, China) and so there has been and probably will continue to be, at least in the short term, a low interest rate environment. I say, in a sense china, because their rate of economic growth is slowing and that is clearly having a negative effect on the Australian economy.

Moving forward, whilst I do believe equities is a better place for higher returns than bonds, I’m not expecting the disastrous returns for bonds that so many commentators are talking about. The Australian economy is transitioning away from a resources-led economic boom and at this stage, there is still nothing there to replace it. Economic growth forecasts aren’t that high and neither should they be. Apart from what I’ve already mentioned, the government appears hardly likely to hand the economy any additional fiscal support and it all adds up to lower levels of average earnings growth too. There are a few other factors I won’t dwell on, but expectations over the next few years should be continued low inflation, low interest rates, low sharemarket returns, and a tough time for the baby boomers as they add fuel to the fire by selling their expensive properties to maintain their retirement lifestyle…so lower residential property returns too.

The one major variable that could change it all is the Aussie dollar. Its currently around $0.88USD and if that continues towards a sustained $0.80USD or below, then the attraction for Australian investment and spending will go beyond the current attraction of higher interest rates and towards industries such as manufacturing, tourism, and our services (e.g. education). But until that happens the investment landscape is bound to be tough…unemployment will continue to increase, our wages will still be globally high, and the spending will continue to be low by recent historic standards.

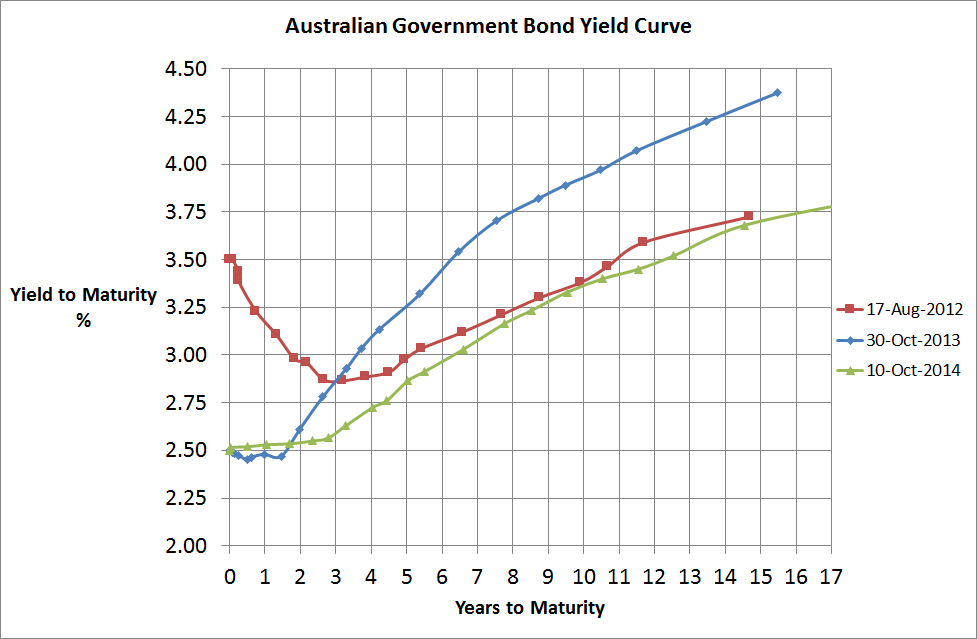

Whilst I don’t believe we’re necessarily heading for any disastrous recession, far from it, I simply believe our complacent view of the Australian economy and expected market returns require an adjustment downwards. And, if you don’t believe me…perhaps you’ll agree with the bond market (see chart below) with government yields suggesting longer term growth expectations are lower than last year and the year before.

Source: Delta Research & Advisory