Background

There’s a widely held belief that to create alpha (i.e. positive returns after adjusting for risk…let’s say market risk), a manager needs to make meaningful bets away from the market. That is, stop being a “benchmark hugger”, concentrate the portfolio with best ideas, and/or move the portfolio holdings away from the benchmark and possibly be more absolute-return oriented. We have all seen numerous strategies that meet these criteria, have generated strong alpha, but is this a reality or it is a belief that is lacking in evidence, save a handful of strategies that just so happen to tell us so. This article seeks to provide some clues to whether accepting greater non-market risk does produce higher alpha.

Non-market risk…and a few technical bits

Firstly, let’s define non-market risk?

Possibly the most frequently used measure is tracking error (which is the standard deviation of the difference between a portfolio’s returns and its benchmark). Whilst tracking error is a good measure of non-market risk, it can be a little misleading in the example of a geared index fund as there is absolute are no bets away from the market due to being an index fund, but the gearing produces a high tracking error. Therefore I believe tracking error creates a potentially inaccurate bias when it comes to comparing non-market risk to alpha generation.

A more recent popular statistic is active share which describes the percentage of holdings that are different to a market benchmark. A portfolio with a high active share suggests a large difference from the benchmark. Because this statistic is a holdings based measure it is quite difficult to measure on a regular basis. Secondly it is also possible to have a portfolio with a high active share but is highly correlated with the market benchmark suggesting that holdings differences do not necessarily translate into performance differences.

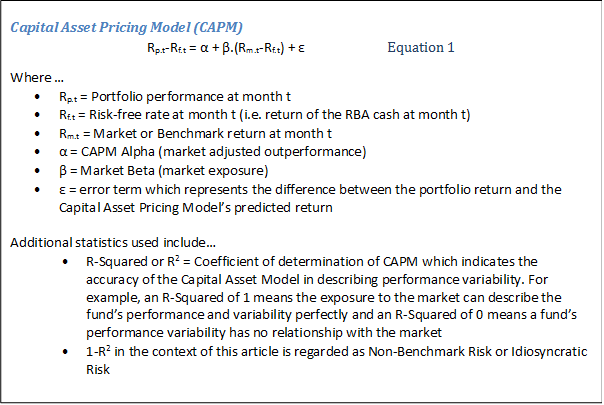

A preferred measure of non-market risk is what some may also call idiosyncratic risk. Idiosyncratic risk is similar to tracking error but is adjusted for exposure to market risk (i.e. market beta) and is defined as the proportion of a total portfolio’s risk due to non-market bets. To be specific, it is (1-R²), where R² is the goodness of fit of the Capital Asset Pricing Model (CAPM) to the portfolio in question … CAPM is represented by Equation 1 below. A second advantage of using idiosyncratic risk is that Equation 1 is also used to calculate Alpha…so a win-win.

So the statistic this paper places most emphasis on is… α/(1-R²)

…and after checking numerous textbooks, I cannot find a name for it, so for this paper will declare it the “Furey Ratio” until someone corrects me. The Furey Ratio is similar to the Information Ratio (which is the ratio of excess benchmark return divided by the portfolio tracking error) but unlike the Information Ratio, the Furey Ratio adjusts for different levels of market risk. So the Furey Ratio is another measure of risk-adjusted return and is Alpha per unit of Idiosyncratic Risk. What we really want to see in an active manager is a high Furey Ratio, meaning they are getting big bang for their non-market risky buck!

Now to the analysis…and a few more technical bits

The analysis plan is to assess whether managers are more likely to produce higher risk-adjusted alpha with greater idiosyncratic risk … so to do this we will test the statistical significance of the Furey ratio, α/(1-R2), from a sample of manager returns.

Data Selection

The manager returns uses performance from two groups of strategies…

- Global Equities (Sample size = 121)

- Australian Equities (Sample size = 226)

…which are the two largest equity asset classes in the Australian investment landscape.

Monthly performance from September 2010 to September 2015 is used and acquired from Morningstar Direct. Duplicated strategies, where the only difference is fee structure, are removed.

The 5 year time-frame to the end of Sep 2015 has been chosen for the following reasons…

- 5 years produces sufficient numbers of both monthly performance (i.e. 60) and number of available strategies

- It is after the Global Financial Crisis period of 2008/09, i.e. from Sep 2010

- It balances the survivorship bias that comes with using a longer time-frame with a reasonable overall sample size…i.e. survivorship bias is a real issue if considering the GFC period as only the better managers survived through to 2015 from before the GFC period

Aside from these reasons, 5 years is still a somewhat arbitrary time period (i.e. it probably makes little difference compared to 5 years and 2 months of data).

Let’s start with Global Equities…

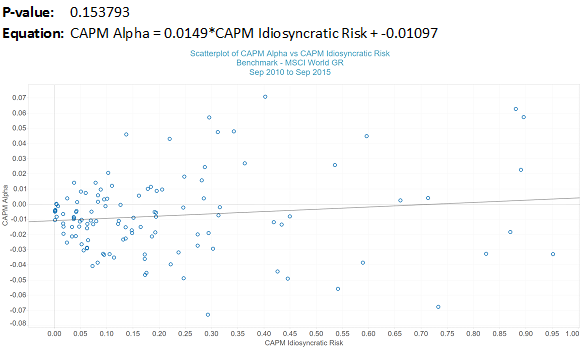

Chart 1 shows CAPM Alpha vs CAPM Idiosyncratic risk over 5 years to end of September 2015 for the 121 Global Equity Managers taken from Morningstar Direct database. All managers chosen have a minimum 5 year track record, and are classified by Morningstar as Global Equities managers.

On the positive side for global equity active managers the regression line in chart 1 slopes upwards suggesting there is a chance that with greater non-benchmark risk comes from higher alpha (CAPM Alpha). This trend demonstrates a positive Furey Ratio but unfortunately, the P-value of 0.153793 of the trend line suggests it is not significantly different from zero at the usual required minimum significance levels (i.e. 0.05)… so weak evidence that higher alpha is not strongly correlated with greater non-benchmark risks.

Chart 1 – CAPM Alpha vs Idiosyncratic Risk – Global Equity Managers (Sep 2010 to Sep 2015)

Source: Delta Research & Advisory

A simple observation from Chart 1 is that there is significant clustering of values at the lower end of the x-axis and a fanning out of alpha levels as Idiosyncratic risk increases. This suggests there may be a reasonable argument that regression analysis of this data may be somewhat inappropriate. So to counteract this issue, the following analysis divides the above CAPM Idiosyncratic risk measure into 5 quintiles.

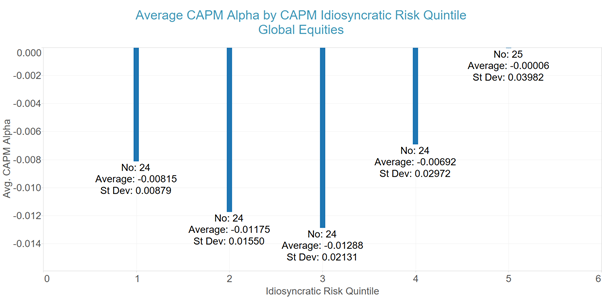

Chart 2 – CAPM Alpha vs Quintiles of Idiosyncratic Risk – Global Equity Managers (Sep 2010 to Sep 2015)

Source: Delta Research & Advisory

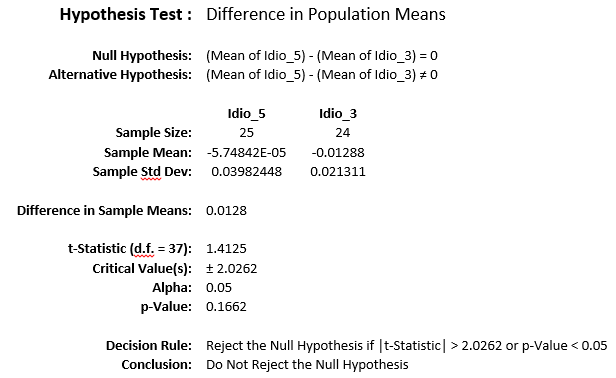

Once again, there are positive signs as there is higher Alpha for the two higher quintiles of Idiosyncratic Risk. However, and unfortunately for active managers, the higher values are not statistically different…please refer the following Hypothesis Test between quintiles 3 and 5 (which have the largest difference).

Source: Delta Research & Advisory

So stopping the analysis of Global Equities strategies there, so far there is little evidence to suggest a statistically significant and positive Furey Ratio amongst the Australian market of Global Equities managers over the last 5 years … therefore suggesting higher idiosyncratic risk probably hasn’t produced higher alpha.

…lets move on to Australian Equities strategies

Similar to Global Equities strategies chosen, a sample of Australian Equity managers have been chosen from the Morningstar Direct database, duplicated strategies have been eliminated, and 5 years of monthly performance between September 2010 and September 2015 used for the following analysis.

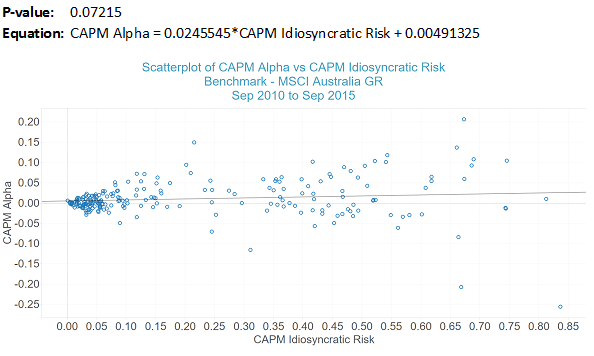

Chart 3 shows that once again there is the spread of Alpha as Idiosyncratic risk increases and the slope of the line (i.e. Furey Ratio) increases. Also similarly, the Furey Ratio is not significantly different from zero at the 5% level (P-value = 0.07215 which is greater than 0.05), also indicating this chart does not suggest greater alpha from higher levels of idiosyncratic risk…at least using statistical tests.

Chart 3 – CAPM Alpha vs Idiosyncratic Risk – Australian Equity Managers (Sep 2010 to Sep 2015)

Source: Delta Research & Advisory

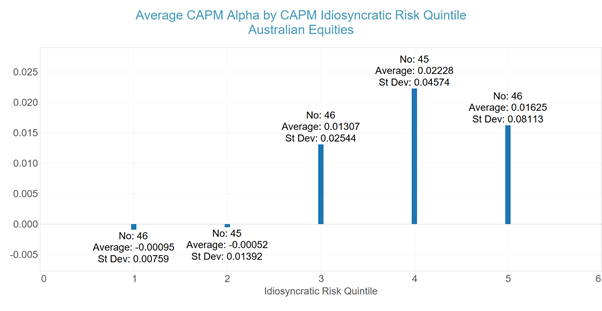

Like Global Equities there is a reasonable argument that the regression analysis is not appropriate due to the larger variance of Alpha as Idiosyncratic risk increases so similar group analysis is applied by dividing Idiosyncratic Risk into quintiles and the results are shown in Chart 4.

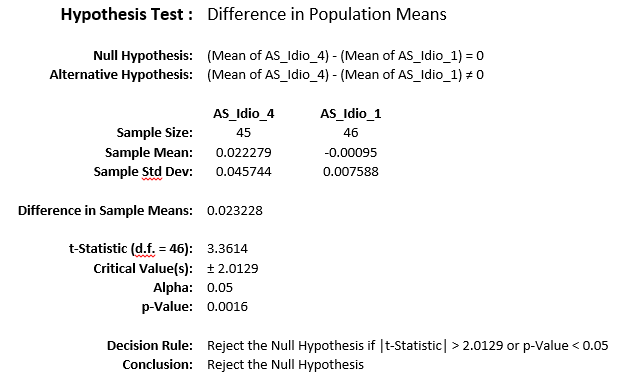

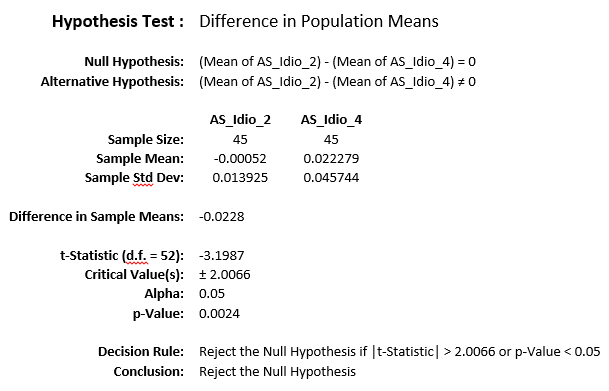

This time there is a statistically significant difference between the Alpha of those managers at the 4th quintile and those at both the first and second quintile…but not between the others (you’ll have to trust me on this)…please refer following Hypothesis Testing results.

Chart 4 – CAPM Alpha vs Quintiles of Idiosyncratic Risk – Australian Equities Managers (Sep 2010 to Sep 2015)

Source: Delta Research & Advisory

Source: Delta Research & Advisory

Source: Delta Research & Advisory

…Stretching the analysis just that little bit further…

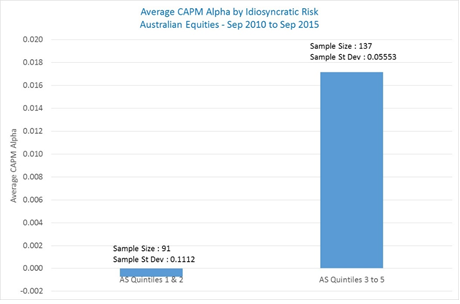

Observing Chart 4, it does appear to show two distinct groups where quintiles 1 and 2 have Alpha results around 0 whilst quintiles 3 to 5 have CAPM Alpha of more than 1% on average…which I’m sure many active managers would be pleased about. Combining the quintiles into these 2 groups yields the following results for CAPM Alpha…

Chart 5 – CAPM Alpha vs Quintiles 1 & 2 and Quintiles 3 to 5 of Idiosyncratic Risk – Australian Equities Managers (Sep 2010 to Sep 2015)

Source: Delta Research & Advisory

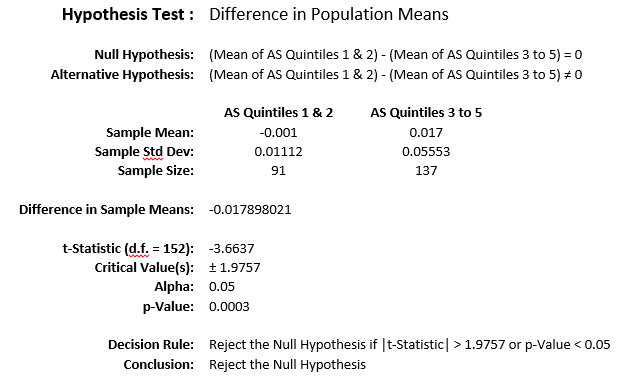

…and the difference in means are statistically significant given the Hypothesis rejection below…

Source: Delta Research & Advisory

So, if I may say that after some potential data mining, there may be some evidence that greater idiosyncratic risk relates to higher levels of alpha (or at the risk of being egotistical, a higher Furey Ratio) among Australian equities managers.

For those interested, the level of Idiosyncratic Risk that intercepts between Quintiles 2 and 3 is only 5.82% (which is around the borderline of the clustering in Chart 3)… meaning if the market, as defined by MSCI Australia GR, explains more than 94.18% (i.e. 1 – 0.0582) of an Australian equity manager’s performance volatility, then this may decrease the chances of generating positive alpha and vice versa.

Conclusion

Over the 5 years to September 2015, the evidence within this paper is possibly weaker than many would expect and shows there is little to no relationship between managers generating alpha and idiosyncratic risk…particularly for Global Equities strategies.

There is some evidence that greater idiosyncratic risk has led to higher alpha amongst Australian Equities strategies although it does not appear to be a linear relationship. However, the result over the last 5 years does show that Australian equities managers have, on average, produced a significantly higher alpha if their non-benchmark risk is greater than around 5.8%.

So for Australian equities managers, the optimistic conclusion (so far) is that there are two groups…the first group is the much-maligned benchmark huggers (with idiosyncratic risk less than 5.8%) who have struggled to produce any alpha at all on average; and the second group with idiosyncratic risk that is higher than 5.8% which has produced a significantly higher alpha of 1.7%pa over the 5 years to September 2015. This result doesn’t mean the higher the idiosyncratic risk the higher the alpha (because of the lack of linear relationship) but it is some evidence that a higher non-benchmark risk does increase the chances of positive alpha…so the jury is still out but benchmark huggers should beware.

2 pings