It appears that the financial planning industry is a big believer in rebalancing but a little unsure as to how often. Some accept the automatic quarterly option, some rebalance at the client review, some annual, or even at 13 months to potentially reduce capital gains tax by taking advantage of the 50% CGT discount.

Because the rebalance decision is often made without a second thought, planners often forget that it is in fact an active decision as to the likely frequency of tops and bottoms of the markets they are investing their clients funds into. For example, if you choose a quarterly option for your client, then in effect, its the same as believing it is likely to be a good decision to sell some equities in 3 months if they have gone up compared to other asset classes or buy some more if they underperformed. This assumption may clearly be wrong and may also have little in common with the asset allocation decision which I expect is typically designed with a longer period in mind. In other words, the asset allocation decision is a recommendation of the most efficient asset allocation for a specified time period and that time period is more likely to be multiple years than one quarter. So by rebalancing every quarter there is the risk of diluting the designed benefit of the asset allocation decision which is made with different goals in mind.

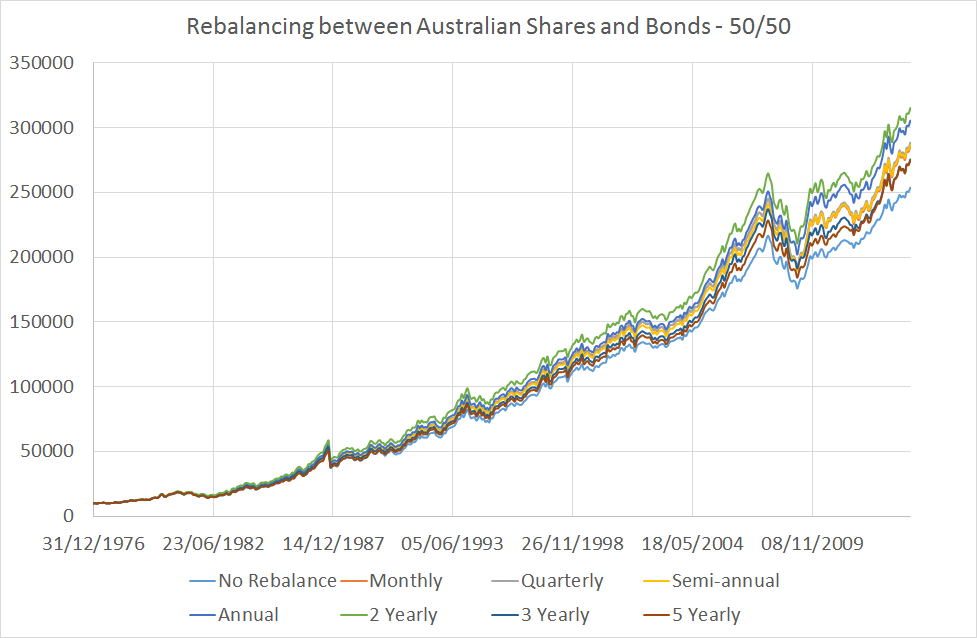

Using just Australian bonds and Australian equities I undertook a little experiment to find out which rebalance frequency may produce the better results. The experiment starts with 50% allocated to Australian Bonds and 50% to Australian equities and I rebalance at various intervals starting from Dec 1976 (that”s how far back my data goes) to see which end up with the best result. For the purposes of simplicity, I ignore tax and transactions costs (which is a very important consideration with real money) and the results are shown in Chart 1 below…

Chart 1

Source: Delta Research & Advisory

Its obviously a fairly close race over almost 40 years so Chart 2 provides a close-up that more clearly shows the winner…

Chart 2

Source: Delta Research & Advisory

…and the winner is the 2 yearly rebalance, with second place going to the annual rebalance and ;last place to “no rebalance”. Now its important to point out that these results are far from complete. Why? because that start date is always 31/12/1976 and the end date always 30/4/2014, and therefore when rebalancing occurs there are some dates (like yearly anniversaries) that are always rebalanced on, whilst the months of Jan, Feb, Apr, May, July, Aug, Oct, Nov never experience a rebalance. So for completion to this experiment different start dates, and rebalance months should be used. As alluded to before, the rebalance decision is a passive decision but essentially is still making a call that it is worth selling one asset and buying another at particular points in time.

Either way, these early results are interesting. A two year rebalance can provide other guaranteed and obvious benefits over monthly, quarterly, six monthly, and annual rebalancing…that is, lower tax consequences and lower transaction costs. Finally, there is no over pattern at this point in time…given the worst results are the less frequent “no rebalance” and 5 year, and the best beating the more frequent rebalancing options…perhaps its suggesting that the stronger performing equity markets are more likely to behave on a 2 year cycle…to be honest, I’m not sure yet.

The early results show 2 years may be best rebalance period but don’t take this for granted and please look out for a completed experiment in the weeks to come.

Please note, I have to admit that I got a little lazy and failed to do any literature search for others that may have written on the rebalancing subject so I hope the early results to this experiment with the latest Australian data still adds a little value to the debate.